UK Landlord Tax Optimization Guide - Part 2: Allowable Expenses & Tax Relief

Written: June 3rd, 2025

Building on Part 1's foundation of core tax obligations and digital requirements, Part 2 focuses on one of the most impactful areas for immediate tax optimization: understanding and claiming all legitimate allowable expenses. This is often where landlords can make the biggest difference to their bottom line through systematic expense management.

Maximizing Deductions: The Power of Allowable Expenses

One of the most direct ways to reduce your taxable rental profit – and therefore your income tax liability – is by claiming all legitimate allowable expenses. Many landlords inadvertently leave money on the table by overlooking smaller expenses or misunderstanding what qualifies for deduction.

The "Wholly and Exclusively" Rule Explained

The cornerstone of claiming expenses against rental income is HMRC's "wholly and exclusively" rule. For an expense to be deductible, it must have been incurred solely for your property rental business. If an expense serves both business and personal purposes, it cannot be claimed in its entirety – but it can often be apportioned.

Understanding apportionment opens up valuable deduction opportunities for expenses that have mixed business and personal use. The key is having a clear, justifiable method for calculating the business portion.

Common apportionment examples include:

Phone bills: If your personal mobile is also used for managing rental properties, you can claim a reasonable proportion of costs related to business use.

Vehicle running costs: When using your personal car for property-related travel like inspections or repairs, you can claim the business portion of fuel, insurance, and maintenance. HMRC offers simplified mileage rates as an alternative to tracking actual costs.

Home office costs: If you run your property business from home, you may claim a proportion of household utilities and council tax based on the area used for business and time spent on property management.

The success of any apportionment claim rests on robust record-keeping and clear documentation of your calculation method. This ensures both HMRC compliance and maximizes your legitimate claims.

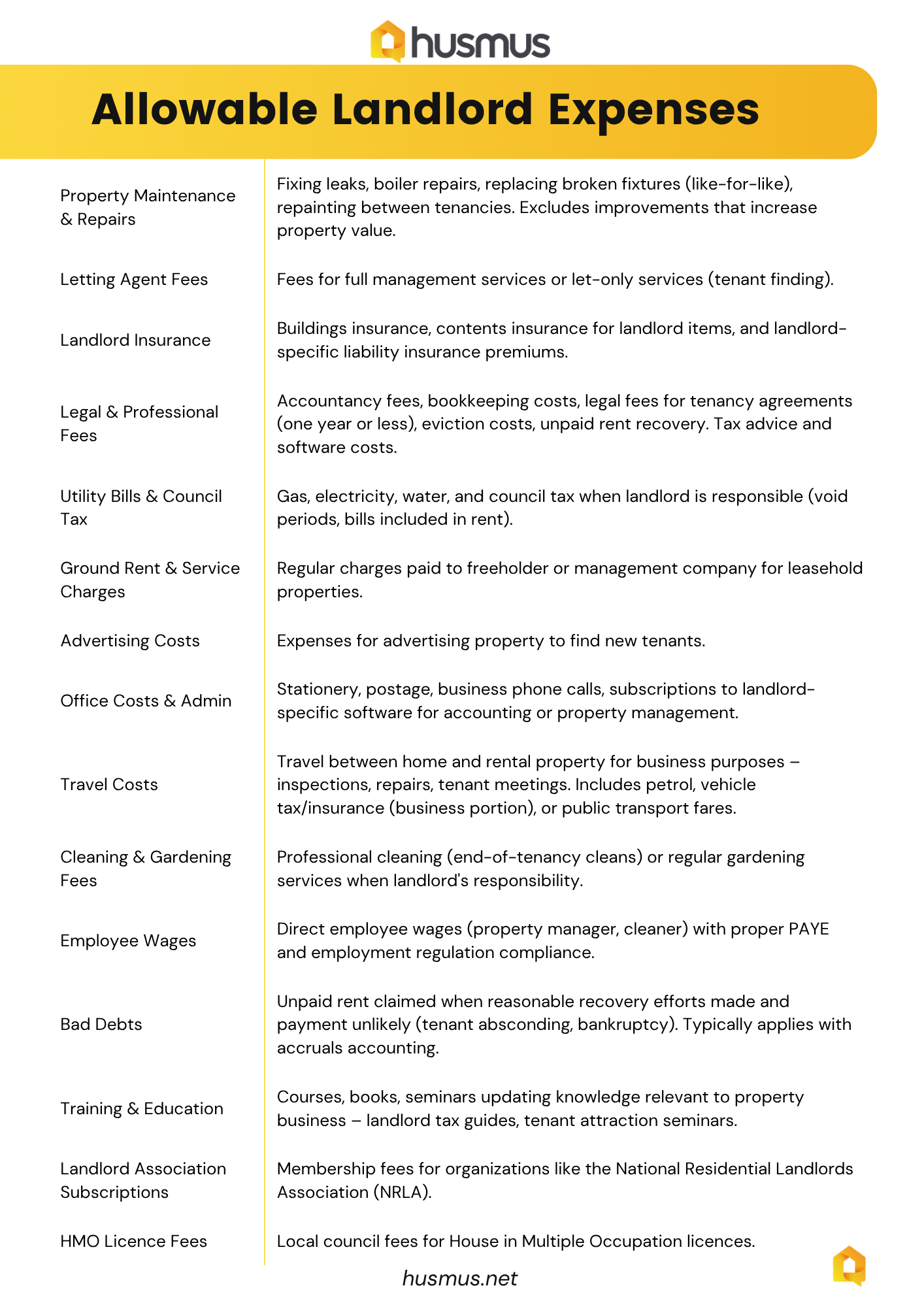

Comprehensive List of Allowable Revenue Expenses

Landlords can deduct a wide array of day-to-day running costs from their rental income. Keeping meticulous records - including all receipts and invoices for at least six years - is essential, as HMRC may request these as evidence.

Claiming these expenses directly reduces taxable rental profit, lowering your overall income tax bill and potentially helping you remain within lower tax bands – avoiding Personal Allowance tapering or higher rate impacts.

Repairs vs. Improvements: A Critical Distinction for Tax Savings

One of the most frequently misunderstood areas involves distinguishing between 'repairs' and 'improvements'. Understanding this distinction correctly can make a meaningful difference to both your immediate tax position and your future Capital Gains Tax when selling property.

Repairs mean bringing an asset back to its previous working condition and count as revenue expenses you can deduct from rental income in the year you incur them. Think of repairs as getting things back to how they were. Examples are

Repainting worn rooms

Fixing leaking pipes or broken windows

Replacing damaged kitchen units with similar standard and quality items

Replacing storm-damaged roof slates

Improvements mean taking an asset beyond its original state, adding value or extending its useful life. These are capital expenses that can't be deducted from rental income immediately, but they can be added to your property's 'base cost' to reduce taxable gains when you eventually sell. Improvements include:

Adding property extensions

Converting lofts into additional bedrooms

Significantly upgrading basic kitchens to luxury specifications

Initial refurbishment of derelict properties to habitable condition

It’s important to note that a principle called the modern equivalent principle often works in your favor here. Replacing items with their modern equivalents usually qualifies as repairs, even when technological advances mean some incidental improvements come along for the ride. Swapping old single-glazed windows for new double-glazing of similar style typically counts as repair work. However, if you're making significant quality upgrades - like replacing standard uPVC windows with bespoke hardwood sash windows - part of that cost might be considered an improvement.

When you're undertaking projects that mix both repairs and improvements, ask your contractors to provide itemized invoices that clearly separate the costs for each type of work. This simple step makes it much easier to allocate expenses correctly for tax purposes and ensures you're claiming everything you're entitled to claim.

Replacement of Domestic Items Relief (RDIR)

Since April 2016, landlords of residential properties have been able to claim Replacement of Domestic Items Relief. This replaced the former 10% 'wear and tear' allowance that was available for furnished properties.

RDIR allows you to deduct the actual cost of replacing domestic items within your let residential property. This relief is available for properties that aren't Furnished Holiday Lettings and where you're not claiming Rent-a-Room relief for the same income.

The types of items covered by RDIR include:

Movable furniture (beds, sofas, tables, wardrobes)

Furnishings (carpets, curtains, linens)

Household appliances (washing machines, fridges, cookers)

Kitchenware (crockery, cutlery, utensils)

The key condition for claiming RDIR is that your replacement item must be broadly of similar standard and quality to the old item – essentially a 'like-for-like' replacement. If you decide to upgrade significantly, the relief you can claim is restricted to what it would have cost to replace the old item with an equivalent, not the actual cost of your upgrade. So if you replace a basic fridge with a high-end American-style fridge-freezer, your deduction would be limited to the cost of a new basic fridge.

The relief calculation includes:

The cost of the new replacement item

Plus any incidental costs of disposing of the old item (removal fees)

Plus any incidental costs of acquiring the new item (delivery or installation fees)

Less any money received from selling or disposing of the old item

It's important to understand that RDIR cannot be claimed for the initial cost of furnishing a property when you first let it out. The relief is specifically for replacement of existing items. You'll need to keep detailed records of the original item being replaced, any proceeds from its disposal, and the cost of the new replacement item to correctly calculate and claim this relief.

Key Tax Reliefs and Allowances for Landlords

Beyond claiming day-to-day expenses, UK tax law provides specific allowances and reliefs that can further reduce your tax liability. Understanding and using these where they apply is an important part of effective tax optimization.

The £1,000 Property Income Allowance

You can benefit from a £1,000 tax-free Property Income Allowance each tax year. How this works depends on your total gross property income:

If your gross property income is £1,000 or less: You don't need to declare this income to HMRC or pay tax on it, provided you don't need a tax return for other reasons. This is known as 'full relief'.

If your gross property income is more than £1,000: You have a choice between two approaches:

Deduct your actual allowable expenses in the usual way

Claim the £1,000 Property Income Allowance as a flat deduction against your gross rental income, instead of claiming actual expenses (this is 'partial relief')

The £1,000 allowance generally works better if your actual deductible expenses for the tax year are less than £1,000. If your expenses are higher than £1,000, claiming your actual expenses will usually be more tax-efficient.

Each joint owner of a property can claim their own £1,000 allowance against their share of the rental income.

There are some situations where you can't use the Property Income Allowance. These include when your rental income comes from a company you own or control, from a business partnership, when you're claiming mortgage interest tax relief under Section 24, or when you're using the Rent a Room Scheme for that income.

The crucial Section 24 interaction you need to know:

If you choose to use the £1,000 Property Income Allowance, you cannot also claim the 20% tax credit on your mortgage interest under Section 24 rules. This is often a critical decision point. For most landlords with buy-to-let mortgages, the 20% tax credit on mortgage interest is likely to be substantial. If this credit, combined with your other actual allowable expenses, exceeds £1,000, then claiming actual expenses (and getting the Section 24 credit) will almost certainly be better than taking the £1,000 flat allowance.

Here's a practical example: if you have mortgage interest payments of £6,000 in a year, your 20% tax credit would be £1,200. Even with no other expenses, claiming the Section 24 credit would be better than taking the £1,000 flat allowance. You need to calculate carefully which option gives you the lower tax bill. This choice affects both your taxable profit calculation and how much record-keeping you need to do – claiming the allowance is administratively simpler if your actual expenses are minimal.

The Rent a Room Scheme

The Rent a Room Scheme provides specific tax relief for individuals who rent out furnished accommodation in their main home.

Under this scheme, you can receive up to £7,500 in gross rental income per tax year completely tax-free if you're an owner-occupier or a tenant sub-letting with permission

This limit halves to £3,750 per person if you're sharing the rental income (for example, if the property is jointly owned and you split the income)

"Gross receipts" for this scheme include the rent you receive plus any payments from your lodger for services like meals, cleaning, or laundry

How the scheme works:

If your gross receipts are £7,500 (or £3,750) or less: The tax exemption is automatic. You don't need to declare this income on a tax return, and no tax is payable. However, if you've made a loss (your expenses exceed your income), it might be worth opting out of the scheme for that year so you can claim the loss against future profits by completing a tax return in the normal way.

If your gross receipts are more than £7,500 (or £3,750): You have two options for calculating your tax:

Method A (Actual Profit): Pay tax on your actual profit, calculated as total receipts minus actual allowable expenses and any capital allowances. This is the default method HMRC will use unless you choose otherwise.

Method B (Tax on Excess over Limit): Pay tax only on the gross receipts that exceed the £7,500 (or £3,750) limit. If you choose this method, you can't deduct any expenses or capital allowances.

You can choose which method to use each tax year and switch between them. If you want to use Method B (or switch back to Method A after previously choosing Method B), you need to inform HMRC, usually via your Self-Assessment tax return, within the statutory time limits. The choice between Method A and B when your income exceeds the threshold requires careful calculation. If your actual expenses are very low, Method B might result in less tax. But if your expenses are significant, Method A could work better for you, even when your gross receipts are above the limit.

You can't use the Rent a Room Scheme together with the £1,000 Property Income Allowance for the same rental income. Also be aware that taking in a lodger under this scheme may affect your entitlement to the single person discount for Council Tax. This scheme is generally more generous than the standard £1,000 property allowance for the specific situation of letting a room within your own main home.

In Part 3, we'll explore Section 24 implications and how to navigate mortgage interest restrictions strategically to maintain your property investment returns.